Your home has seen it all—the late-night snack runs, the family movie nights, and the time your dog decided to redecorate the living room with muddy paw prints. But if your walls could talk, they might have a few things to say about your home insurance policy—and not all of it would be good news.

Most homeowners assume their policy covers everything. However, many policies have gaps that could leave you footing a hefty bill when disaster strikes. Let’s take a peek behind the drywall and uncover what your home insurance won’t tell you.

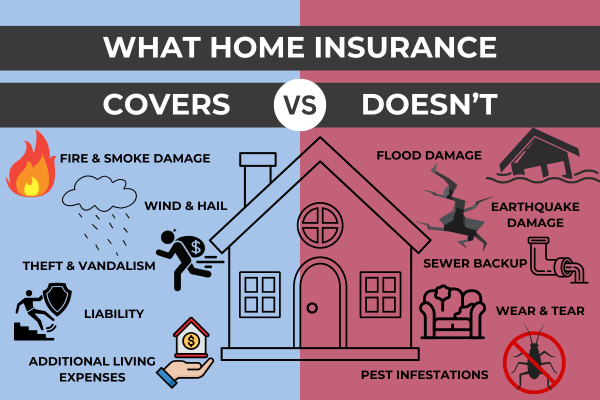

- “I May Not Cover That Flood in the Basement.”

Water damage is one of the most common home insurance claims, but not all water-related incidents are covered.

- Flood damage? That requires a separate flood insurance policy. Learn more from the National Flood Insurance Program.

- Sewer backup? You need an add-on for that.

- Leaky pipes over time? Most policies only cover sudden and accidental water damage, not slow leaks.

💡 Solution: Check if you need a sewer and drain water damage endorsement—especially if you live in a high-risk area. You can also explore coverage options with Farmers Home Insurance. Additionally, consider installing a leak detection system like the Moen Flo Smart Water Monitor and Shutoff to help prevent costly water damage. This device detects leaks in real time and can automatically shut off the water to prevent flooding.

- “Your Valuables Might Be Worth More Than I Can Cover.”

Think your homeowner’s policy fully protects your jewelry, collectibles, or expensive electronics? Think again. Most standard policies have low limits on high-value items—often $1,500 or less for jewelry and electronics. For more information, check out this guide on scheduled personal property endorsements.

💡 Solution: Get a scheduled personal property endorsement to cover high-ticket items properly.

3. “Renovations? I Hope You Told Me!”

If you’ve upgraded your kitchen or built an addition, congratulations! However, if you didn’t notify your insurance company, your policy may not reflect your home’s actual value—meaning you could be underinsured in a disaster.

💡 Solution: Always update your policy when making major home improvements to ensure your coverage keeps up with your home’s value. Contact your insurance provider before starting renovations to discuss potential coverage adjustments and avoid being underinsured.

4. “Replacement Cost and Actual Cash Value Are NOT the Same.”

Many homeowners assume they’ll get a brand-new replacement for damaged belongings—but policies vary.

Replacement Cost: Covers the full cost of replacing an item with a new one.

Actual Cash Value: Pays out the item’s depreciated value, which could be way less than what you paid.

💡 Solution: Opt for Replacement Cost Coverage whenever possible to avoid unexpected financial gaps. Need help choosing the right policy? Get a free quote today.

Final Thoughts: Listen to Your Home Before It’s Too Late

Your home may not be able to talk, but your insurance policy can—if you ask the right questions. Reviewing your coverage regularly ensures you’re protected from the unexpected.

If you’re unsure whether your policy has gaps, reach out today for a free policy review—because when disaster strikes, you don’t want any surprises.