Life insurance isn’t just about having a policy—it’s about having the right policy. And when it comes to choosing between Term Life Insurance and Permanent Life Insurance, the decision isn’t as simple as picking one over the other. Each serves a different purpose, and the right choice depends on your goals, your future, and how you want to use your coverage.

So let’s cut through the jargon and get to the real difference between these two policies—because understanding your options means making smarter decisions for yourself and the people who matter most.

TERM LIFE: SIMPLE, AFFORDABLE, AND STRAIGHT TO THE POINT

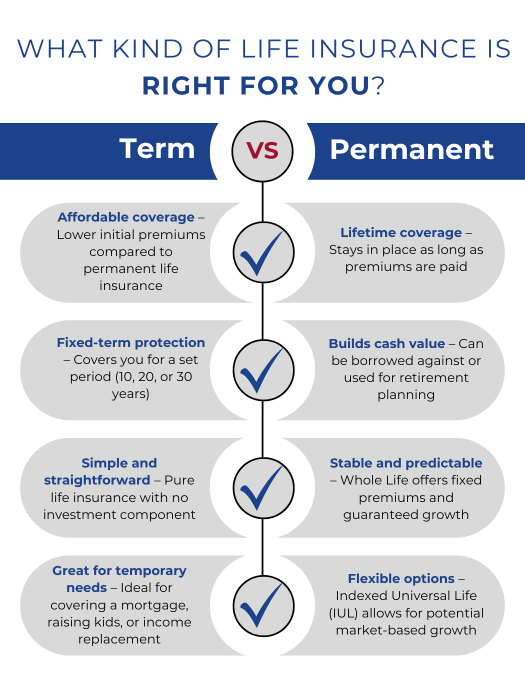

Think of Term Life Insurance like renting a home. You get coverage for a set period (usually 10, 20, or 30 years), and if you pass away during that time, your beneficiaries receive a tax-free payout (called the death benefit). But when the term is up, the coverage ends unless you renew or convert it.

Why Choose Term Life?

- It’s affordable – Term life is the least expensive way to get high coverage.

- It’s straightforward – You pay premiums, and if you pass within the term, your family is financially protected.

- It’s great for temporary needs – Perfect for covering a mortgage, raising kids, or replacing income if you pass away early.

Potential Downsides:

- No cash value – If you outlive the term, you get nothing back.

- Increasing premiums – If you renew after the term expires, costs can go way up.

- No flexibility – It’s a simple death benefit with no investment component.

PERMANENT LIFE INSURANCE: COVERAGE THAT LASTS A LIFETIME

Permanent life insurance is different—it’s meant to last your entire life as long as you pay your premiums. It also includes a cash value component, which can grow over time. There are two main types: Whole Life Insurance and Indexed Universal Life (IUL).

WHOLE LIFE INSURANCE: GUARANTEED PROTECTION AND FIXED GROWTH

Whole life insurance is the most traditional form of permanent coverage. It offers guaranteed benefits, including:

- Fixed premiums – Your payments stay the same for life.

- Guaranteed cash value growth – The cash value grows at a set rate, so there’s no risk of losing money.

- Lifetime coverage – The policy stays in place as long as you continue paying premiums.

While whole life insurance is stable and predictable, it tends to be more expensive than term life, and the growth potential of the cash value is relatively low compared to other options.

INDEXED UNIVERSAL LIFE (IUL): PROTECTION WITH GROWTH POTENTIAL

Indexed Universal Life (IUL) offers lifetime coverage like whole life but adds a unique feature: the ability to grow cash value based on stock market indexes like the S&P 500.

Why Choose IUL?

- Flexible premiums – You can adjust your payments over time.

- Cash value growth potential – The cash value can increase based on market performance, offering greater earning potential than whole life.

- Tax advantages – The cash value grows tax-deferred, and you can access it through policy loans.

- No market risk on cash value – Even if the stock market drops, your IUL has a “floor,” meaning you won’t lose money due to negative returns.

Potential Downsides:

- Higher cost – Permanent policies, including IUL, are more expensive than term life.

- Complexity – IUL isn’t a “set it and forget it” policy; it requires some management.

- Cash value takes time to build – It won’t accumulate immediately but grows over the long term.

WHY CHOOSE FARMERS INSURANCE?

Farmers Insurance offers a range of life insurance products that cater to different needs and financial goals. Whether you need affordable term coverage, a guaranteed whole life policy, or an IUL that grows with your future, Farmers provides:

- Customizable policies – Tailor your coverage to fit your specific financial and family needs.

- Trusted financial strength – Backed by years of experience and a strong reputation in the insurance industry.

- Exceptional customer service – Get guidance from experienced agents who help you understand your options and make informed decisions.

- Flexible riders – Add options like accelerated death benefits, waiver of premium, and child coverage to enhance your policy.

WHICH ONE IS RIGHT FOR YOU?

Term Life may be a good choice if:

- You need affordable, high coverage for a specific period (like while raising kids or paying off a mortgage).

- You just want straightforward protection without investment features.

- You have a tight budget but still want to protect your loved ones.

Permanent Life may be a good choice if:

- You want lifetime coverage that never expires.

- You like the idea of building cash value over time.

- You want the flexibility to borrow against your policy or use it for supplemental retirement income.

- You’re thinking long-term financial planning and want an insurance policy that works as an asset.

FINAL THOUGHT: IT’S NOT ONE-SIZE-FITS-ALL

Life insurance isn’t just about what happens after you’re gone—it’s about how you plan for your future today. If you want simple, affordable coverage for a set period, Term Life is the way to go. But if you’re looking for lifelong protection with financial growth, Permanent Life Insurance—whether Whole Life or IUL—might be worth considering.

Still not sure? Let’s talk. The best policy is the one that truly fits your life, goals, and budget.